What Is a Crypto Factor Stack? Combining Funding, OI, Volume, Regime, and Breadth

A plain-language explanation of a crypto factor stack: what a factor is, why combining funding, open interest, volume, regime, and breadth beats any single indicator, and how an honest desk records whether the stack is working.

Summary

A factor stack is a way of scoring a market on several independent dimensions at once, instead of trusting one indicator to carry the whole decision. For crypto perpetuals the natural factors are funding, open interest, volume, regime, and breadth.

This explainer covers what a factor is, why stacking factors is more robust than chasing a single signal, the failure modes to respect, and why the only honest way to run a stack is to record whether it has actually worked.

What "factor" means, without the jargon

A factor is one measurable dimension of a market that carries information about it. On its own, a factor is rarely a decision; it is one reading among several. Price momentum is a factor. Funding is a factor. So are open interest, traded volume, the broad market regime, and breadth across the universe. A factor stack is simply the practice of measuring several of these at once and combining them into a single score, so no single dimension gets to decide alone.

The reason this matters is that any one indicator can be loud and wrong. A market can be ripping on momentum while funding screams that the move is already crowded. Open interest can be climbing while volume quietly thins out, which is a different and more fragile picture than open interest climbing on rising participation. A single-factor view forces you to pick which lens to trust and then live with its blind spots. A stack lets the factors check each other.

The crypto-native factors and what each one carries

On perpetual futures, a small set of factors does most of the work, and each answers a distinct question.

Read alone, each of these is a half-truth. Read together, they describe a fuller picture: not just that a market is moving, but whether the move is clean, crowded, broad, supported by volume, and consistent with the regime.

- Momentum and relative strength ask whether the market is moving and whether it is leading or lagging its peers. This is the part a chart screener handles well, and it is the entry point, not the conclusion.

- Volume asks whether the move has participation behind it. A move on thin volume and a move on heavy volume can look identical on price and mean opposite things about how durable it is.

- Funding asks who is paying to hold the position. Persistently rich funding tells you the crowd is already leaning one way and is paying for the privilege, which is information about how crowded, not how strong, the move is.

- Open interest asks how much positioning has actually accumulated, because open interest is the stock of contracts that eventually has to unwind. The interaction between a price move and the open interest behind it is one of the richest readings in the whole stack.

- Regime asks what kind of market you are in at all: trending or chopping, expanding or compressing, risk-on or risk-off at the index level. The same single-factor reading means very different things in different regimes.

- Breadth asks whether the move is broad or isolated, because a single coin running while the universe is flat is a different story than a universe lifting together.

Why stacking beats chasing a single signal

The case for a stack is robustness, not magic. Independent factors fail at different times and for different reasons, so combining them tends to be steadier than leaning on the best-looking single signal, which is usually the one that happened to work most recently. A stack also resists the trap of optimizing one indicator until it looks perfect on history, because the score has to satisfy several dimensions at once rather than being tuned to flatter one.

Stacking is not a guarantee, and it is important to say so. Factors can be correlated, so adding more of them does not always add proportionally more information; five readings that all really measure the same thing are closer to one factor wearing five hats. Factors also drift as market structure changes, so a stack that described the market well in one regime can degrade in another. And a stack is only as honest as the record kept on it. The whole exercise collapses if the factors are weighted by hindsight to fit the trades that already worked.

How an honest desk runs a stack

This is where methodology has to meet accountability. A factor stack produces a score, the score produces a short list of observations, and the only way to know whether the stack is any good is to record what those observations did over time, in public, with wins and losses kept at equal weight and the sample size visible. A stack you can only judge by its winning examples is indistinguishable from a stack that got lucky.

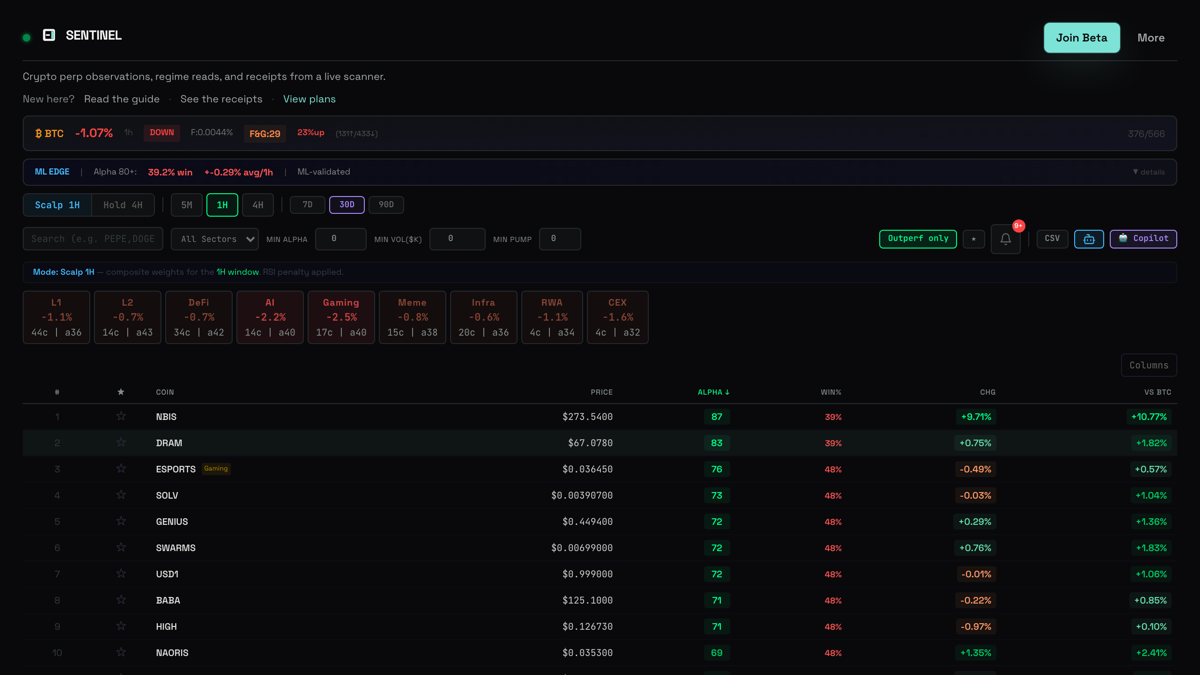

SENTINEL is built around exactly this factor stack — momentum, volume, funding, open interest, regime, and breadth combined into one score per Bybit perpetual — and resolved CORE observations land on public receipts. That standard cuts both ways on purpose: when the recent CORE cohort is weak, the performance page should report that plainly instead of quietly reweighting the factors until the page turns green. A factor stack is a process, not a promise, and the receipts are how you tell the difference. Nothing here is financial advice, and a published record is not a forecast; it is the evidence that lets you decide whether the process deserves your attention.

Common questions

What is a crypto factor stack in simple terms?

It is a way of scoring a market on several independent dimensions at once — for perpetuals, typically funding, open interest, volume, regime, and breadth alongside momentum — and combining them into a single score, so no single indicator gets to decide alone.

Why combine factors instead of using one good indicator?

Any single indicator can be loud and wrong, and the best-looking one is usually whatever worked most recently. Independent factors fail at different times, so combining them is generally steadier and resists tuning one indicator until it flatters past trades.

What are the main weaknesses of a factor stack?

Factors can be correlated, so adding more does not always add proportional information; factors drift as market structure changes, so a stack can degrade across regimes; and a stack is only as honest as the public record kept on it, since hindsight weighting can make any stack look good.

How do I know a factor stack actually works?

Look for a recorded outcome: a public ledger of what the stack surfaced, with wins and losses at equal weight and the sample size shown. A stack you can only judge by its winning examples is indistinguishable from one that got lucky.

Try it live

Connect wallet first, then continue with Telegram to unlock trial/Core features.

How this was produced

Every claim was verified against the live SENTINEL codebase and the current product surfaces. This is educational product documentation, not financial advice.