Funding Rate + Open Interest Scanner: Reading Crowded Bybit Perps

How to read a funding rate and open interest scanner on Bybit perpetuals, what crowded actually looks like, and where regime context turns the signal on or off.

Summary

A funding rate and open interest scanner is most useful when the two columns are read together. Funding alone says what one side is paying; open interest alone says how much capital is committed. Together they describe how crowded a Bybit perp actually is, and that is the question most traders are really asking when they go looking for a scanner.

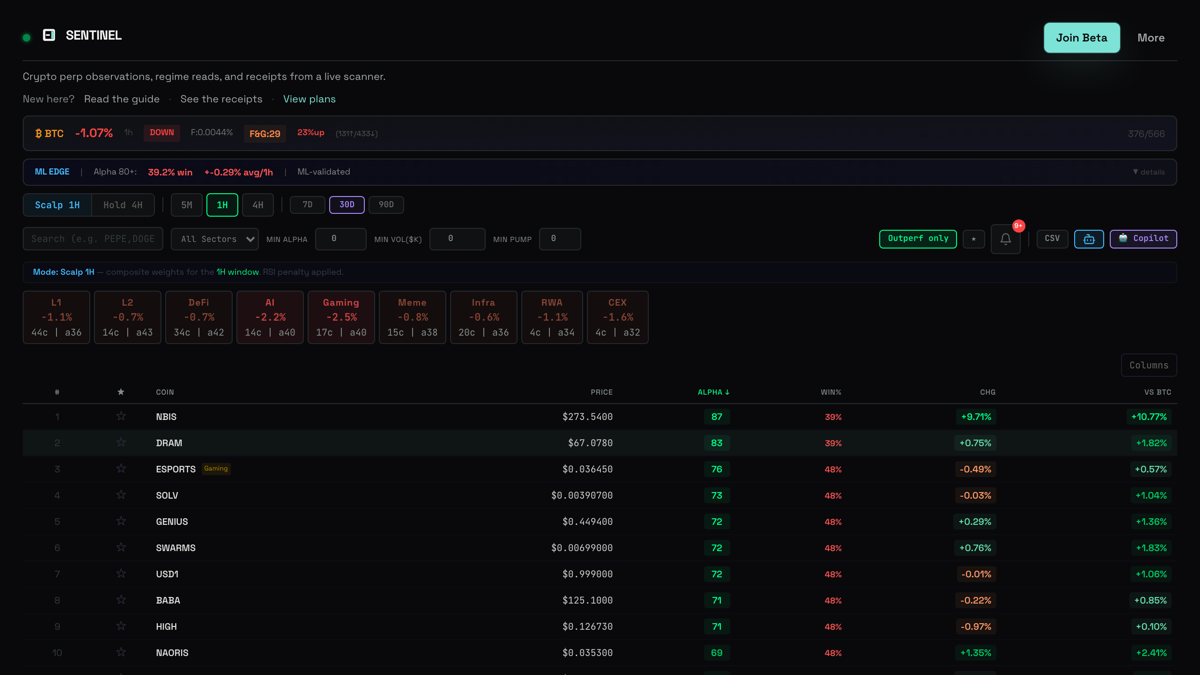

SENTINEL ranks Bybit perpetuals across funding, open interest, volume, momentum, and a cross-market regime gate, and keeps the public CORE receipt window visible before anyone joins the Telegram beta.

Why funding and open interest belong on the same scanner

Traders search for a funding rate and open interest scanner for a specific reason. They have already seen a price chart, and now they want to know whether the move was funded by fresh positioning or extended by leverage on one side of the book. Funding and open interest are the two cleanest signals that the exchange itself publishes for that question, and reading them in isolation usually gets the answer wrong.

Funding tells you which side is paying to maintain its exposure. Open interest tells you whether contracts are being opened or closed. Either column on its own can mislead. A spike in funding with no change in open interest is a different story from a spike in funding while open interest is climbing, and both are different again from a funding spike while open interest is falling. A scanner that hides one of these columns is hiding the part of the story a trader needs.

SENTINEL treats these two columns as a pair. The scanner reads them together at observation time, and the cross-market regime gate decides whether the read is even allowed to escalate into a Telegram alert. That ordering matters more than any single threshold, and the broader Bybit perp scanner factor stack guide on the blog walks through the rest of the columns that interact with this pair.

What funding rate actually measures

On a Bybit perpetual contract, funding is the periodic payment that keeps the perp price tethered to the spot index. It is settled every eight hours and is paid from one side of the contract to the other. Positive funding means longs are paying shorts; negative funding means shorts are paying longs. The size of the payment grows as the spread between the perp and the index widens, which is the exchange's way of pricing the cost of one-sided positioning.

Read at face value, the funding number is a small fee. Read as market microstructure, it is a price the crowd is willing to pay to stay positioned. When that price gets high, it does not by itself predict a reversal. It tells a trader that the move now has to keep proving itself against an explicit periodic cost. Outside catalysts can absolutely sustain that cost; many trends do. The point is to know the cost is there before assuming the move is free.

Funding is also useful as a measure of how unanimous a directional view is across the perp universe. When funding across the top liquid contracts skews hard positive for several settlements in a row, the universe is leaning long in a way that has to be paid for. That description does not predict the next move. It describes the cost structure the next move has to navigate.

- Positive funding: longs pay shorts; the perp is trading above the index.

- Negative funding: shorts pay longs; the perp is trading below the index.

- Funding is a recurring cost on the side that is paying, not a forecast on its own.

- Funding extremes are most informative when paired with open interest and volume context.

What open interest actually measures

Open interest is the total notional value of contracts that are currently open on a Bybit perpetual market. Every long has a short on the other side, so open interest counts the size of the position book, not net direction. When open interest rises, new positioning is entering. When it falls, positions are closing.

The intuition most traders carry around is right but incomplete. Rising open interest during a move means there is new conviction on at least one side. Falling open interest during a move means contracts are being unwound. Neither pattern is good or bad without price context. A clean +3% move with rising open interest is usually broad participation. The same +3% move with falling open interest is more likely position closure, often short covering, and often faster to fade once the forced flow runs out.

A useful scanner does not hide open interest behind a single colour. It reports the delta beside the price change so the reader can quickly classify the move as expansion or contraction. The crypto perp scanner overview elsewhere on the blog walks through the same column in a more general crypto perp setting, and the principle carries cleanly into the Bybit-specific read.

The four-quadrant read: price × OI × funding

Once funding and open interest are visible together, the scanner output becomes a small matrix the reader can hold in their head. Four broad quadrants cover most of what shows up on a Bybit perp, and naming them explicitly makes the read faster during a live session.

The point of the matrix is not to mechanise the trade. It is to give the trader a shared vocabulary for what they are looking at, so the next column on the scanner (volume, momentum, regime) can be checked against a clear hypothesis instead of a hunch. Most weak setups fall out at this stage simply because they do not fit a coherent quadrant.

- Price up, OI up, calm funding: broad participation, new longs entering, no obvious crowding yet. The most durable shape on a perp.

- Price up, OI up, hot funding: longs are crowded and paying for it. The move needs a catalyst to keep going; reset risk rises.

- Price up, OI down: short covering or position unwind. Often sharp, often a bad place to chase, often faster to fade once forced flow clears.

- Price down, OI up, hot negative funding: shorts crowded and paying. A short squeeze candidate, but only if regime supports the rebound.

Where regime gates the funding/OI read

The same funding and open interest pattern can mean different things under different market regimes. A crowded long in a strong, broad uptrend is dangerous but often slow to resolve. A crowded long during a hostile BTC tape with thin breadth tends to resolve faster and harder, because there are fewer marginal buyers to absorb a forced unwind. A scanner that ignores regime keeps the same alert behaviour in both states and lets the user do the filtering. A scanner that respects regime narrows what is eligible when the wider tape is not supportive.

SENTINEL keeps a cross-market regime read that combines BTC trend, breadth across the perp universe, BTC dominance, volatility proxy, and macro context. The reading the crypto regime article on the blog walks through how those legs combine. The funding and open interest read sits inside that gate rather than around it; eligible observations narrow when breadth is thin, and broaden again when the tape supports it.

For the funding/OI read specifically, the regime gate decides whether a crowded read is treated as "crowded continues" or "crowded resets sooner". Either label can be wrong on a given setup; the gate exists to keep the threshold for trusting the read appropriate for the tape, not to remove the trader's judgement.

What "crowded long" actually looks like in practice

The phrase "crowded long" gets used loosely. In factor terms, a Bybit perp is starting to look crowded when funding has been elevated and positive for multiple consecutive funding windows, open interest has built across the same period without a meaningful drawdown, and recent volume has been a chase up into the high of the range rather than a base building below it. None of these conditions is a forecast on its own. Together they describe a position book that is one-sided and paying for the privilege.

A useful scanner does not say "this is crowded, do not buy". A useful scanner says "this is crowded, and here is the rest of the factor stack so you can decide whether the move still has a tailwind". Sometimes crowded continues because the underlying catalyst is real. Sometimes it resolves into a fast reset. The job of the scanner is to make the read legible, not to remove the decision.

- Multiple consecutive positive funding windows, not just one print.

- Open interest expansion through the same window without a clean shake-out.

- Recent volume profile clustered into the high of the range rather than below it.

- Cross-market regime that does not actively support continuation (thin breadth, weak BTC).

Common funding-and-OI misreadings

A few specific misreadings show up so often that they deserve to be named directly. The first is confusing a single high funding print with a sustained crowded regime. One eight-hour window of elevated funding is not a position book; it is one data point. Crowded reads earn their name only when multiple consecutive windows agree and open interest has not been shaken out between them.

The second is assuming that falling open interest during a price move is bearish. It is not bearish on its own. Falling open interest into a green move means contracts are being unwound, which is usually short covering. That can extend further than expected when the shorts being squeezed were sized aggressively, and it can also fail quickly once the forced flow clears. The same column reads differently depending on which side is being unwound.

The third is treating funding as a clean leading indicator for the next eight hours. Funding is a transfer that already happened; it describes the state of the book up to the most recent settlement, not the state of the book in the next window. A scanner that uses funding as a forecast on its own will be wrong often. A scanner that uses it as positioning context inside a larger factor stack will be more useful more of the time.

- One high funding print is a snapshot, not a regime.

- Falling open interest into a green move is unwind, not weakness.

- Funding describes the past window, not the next one.

- Crowded reads need agreement across multiple windows and the surrounding factor stack.

How SENTINEL surfaces funding and open interest

SENTINEL reads exchange feeds server side and grades each Bybit perpetual across price action, momentum, relative strength, volume ratio, funding, open interest, RSI, liquidation pressure, and the cross-market regime read. Funding and open interest sit as first-class columns beside the score, not buried in a tooltip, because the whole point of putting them on a scanner is that the reader can compare them at a glance.

Observations only escalate into a Telegram CORE alert when the factor stack agrees and the regime gate allows it. That is why subscribers get fewer notifications than a typical signal channel and why each one carries the funding, open interest, and regime context attached. The Telegram crypto scanner guide on the blog covers what subscribers actually receive and why the delivery surface is split between the public website and the Telegram bot.

A subscriber receiving a SENTINEL observation should be able to read the funding and open interest context in under five seconds. That constraint shapes how the copy is written. The line that describes positioning carries the funding direction, the recent open interest delta, and a one-word regime label, without trying to dress the data up as a forecast.

How funding and OI interact with liquidations

A crowded long that finally resolves often does so through a liquidation cascade rather than a slow drift. Funding and open interest set the conditions; liquidations describe the event. A scanner that reads all three columns can tell the difference between a clean fundamental move and a forced unwind that looks like one in the first few seconds.

The Bybit liquidation alerts and cascade context article on the blog goes deeper on what a heatmap can and cannot show, and where SENTINEL's liquidation pressure column fits into the rest of the factor stack. The short version: liquidations are the event, funding and open interest are the conditions, and reading the event without the conditions tends to produce late entries.

Receipts before the Telegram trial

Any scanner that reaches Telegram should be inspectable before a trader joins. SENTINEL keeps a public CORE receipt surface that includes the sample size, the wins, the losses, and the worst row of the current measurement window. Live numbers are published at https://sentinelresearch.app/api/scanner/tier-performance?mode=live and surfaced on the public performance page. The goal is not to brag about a single screenshot; it is to let a trader audit the workflow against published outcomes before paying for anything.

Receipts are not promises. They are the record a trader can read with their own eyes, then decide whether the Telegram trial earns their attention. Performance language in any SENTINEL surface is qualitative or cites the live endpoint with a UTC timestamp, because a number quoted in a blog post is already stale by the time it is read.

Risk boundary — what this scanner is not

SENTINEL is a research and observation tool. It does not place trades, manage position size, set stops, manage leverage, or offer financial advice. Bybit perpetual futures are leveraged products and can lose more than the margin posted on a single trade. Funding and open interest are context, not instructions.

If a funding rate and open interest scanner ever sounds like it cannot be wrong, that is the moment to stop trusting it. Read the full risk disclosure before using the Telegram beta, and never let a scanner column define risk for you.

Common questions

Why should funding and open interest be on the same scanner?

Either column on its own can mislead. Funding tells you which side is paying to maintain exposure; open interest tells you whether contracts are being opened or closed. A scanner that hides one of these columns is hiding the part of the story a trader needs.

What does funding rate actually measure on a Bybit perp?

Funding is the periodic payment that keeps the perp price tethered to the spot index, settled every eight hours. Positive funding means longs pay shorts; negative funding means shorts pay longs. It is a price the crowd is willing to pay to stay positioned, not a forecast on its own.

What does open interest measure?

Open interest is the total notional value of contracts that are currently open on a Bybit perpetual market. Every long has a short on the other side, so open interest counts the size of the position book, not net direction. Rising means new positioning is entering; falling means positions are closing.

What is the four-quadrant read on price, OI, and funding?

Price up, OI up, calm funding is broad participation. Price up, OI up, hot funding is crowded longs paying for the move. Price up, OI down is often short covering or position unwind. Price down, OI up with hot negative funding is a short-squeeze candidate, but only if regime supports the rebound.

What does "crowded long" actually look like in factor terms?

Funding elevated and positive for multiple consecutive windows, open interest built across the same period without a meaningful drawdown, recent volume clustered into the high of the range rather than building a base below it, and a cross-market regime that does not actively support continuation.

What are the most common funding-and-OI misreadings?

Confusing a single high funding print with a sustained crowded regime, assuming that falling open interest during a green move is bearish when it is usually unwind or short covering, and treating funding as a clean leading indicator for the next eight hours when it actually describes the window that just settled.

Try it live

Connect wallet first, then continue with Telegram to unlock trial/Core features.

How this was produced

Every claim was verified against the live SENTINEL codebase and the current product surfaces. This is educational product documentation, not financial advice.