Bybit Funding Rate Alerts: When Crowded Pays You, When It Doesn't

How to read Bybit funding rate alerts honestly: when crowded positioning is a fade candidate, when it is a tailwind, and what context kills both reads.

Summary

Funding rate alerts on Bybit get marketed as a contrarian edge: crowded positioning pays, fade the extremes. In practice that edge is unstable until funding is read alongside open interest, volume, and the broader market regime.

SENTINEL treats funding as one column inside the factor stack. The Telegram delivery surface only escalates observations when the columns agree and the regime gate allows it.

The trader who searches for funding alerts

A trader searching for Bybit funding rate alerts has usually already heard the simple version. Funding goes positive when longs pay shorts; when it gets high, the trade is crowded; fade the crowd; collect. That version is half-true. It is right that funding describes positioning pressure. It is wrong that the funding number alone tells a trader when the crowd is about to break.

The alerts that ship in most products are a thin layer on top of that half-truth. They notify the trader when funding crosses a threshold. They do not say whether open interest is rising or falling, whether the volume profile supports a continuation or a fade, or whether the regime is supportive of either direction. A serious funding alert needs that context attached or it becomes another notification a trader has to filter manually.

The buyer profile for this article is the trader who has already tried threshold-based funding alerts and noticed how often they are wrong. The point is not to dismiss funding; it is to put the funding number back inside the factor stack where it earns its keep.

How Bybit funding actually pays

On Bybit, funding settles every eight hours and is calculated from the spread between the perp mark price and the underlying index, with an interest-rate adjustment baked in. Positive funding means longs pay shorts; negative funding means shorts pay longs. The size of the payment grows when the perp deviates further from the index, which is the mechanism that nudges the contract back toward fair value.

A trader collecting funding on the short side of a hot positive funding regime is not earning a free yield. They are taking on the risk that the move continues against them long enough that the funding income does not cover the position's drawdown. The same applies in reverse for long-side traders collecting negative funding during a panic. Funding is a periodic transfer; it is not a hedged return.

The eight-hour cadence matters too. A trader who enters a position five minutes before a funding settlement is closer to a transfer event than a trader who enters the same position immediately after one. That timing detail does not change the trade thesis, but it changes the short-term cost structure in a way that some funding alerts ignore entirely. A useful product surfaces the time-to-next-funding alongside the rate so the trader can decide whether the upcoming settlement matters for their entry.

The "crowded pays" trade in theory

The theory behind a fade-the-funding trade is straightforward. When funding has been hot positive for multiple consecutive windows and open interest has expanded into the run, the position book is one-sided and paying for the privilege. A move that fails to extend produces a reset: longs unwind, often with leverage forcing the door, and the price falls back toward where the funding spread was sustainable. The fade trade tries to be on the right side of that reset.

On paper, the trade has a tailwind. In practice, the same pattern can run for days before resolving, can extend into an even more crowded state before any meaningful unwind, and can resolve through a slow drift rather than a sharp reset that the fade trader can profit from. Funding alerts that ignore those failure modes oversell the edge.

The version of the trade that does the worst is the one entered after a single high funding print, with no check on whether open interest is still expanding or has begun to roll. That version is essentially a bet on mean reversion without any of the structural context that makes mean reversion plausible. The trade can still work, but the trader is paying for an option they did not price correctly.

Why it fails in practice (without context)

The most common reason a funding fade trade fails is that the trader entered on the funding signal alone. Funding can stay elevated for long stretches when the underlying narrative is strong. Open interest can keep building. Volume can support continuation rather than a fade. Breadth across the rest of the perp universe can be wide enough that the move has a structural tailwind beyond positioning.

A funding alert that fires every time the rate crosses a threshold is going to be wrong a lot. Not because the threshold is wrong, but because the threshold is a single column. The trader needs the surrounding factor stack to decide whether this particular crowded read is the kind that resets or the kind that grinds on.

- Strong narrative + rising open interest + wide breadth: crowded continues.

- Weak narrative + flat open interest + thin breadth: crowded resets faster.

- Hot funding into a low-volume profile: continuation more likely than reset.

- Hot funding into a volume cluster at the high of the range: reset risk is meaningful.

What context makes the funding fade tradeable

The funding fade becomes more tradeable when the rest of the stack agrees. The setup that tends to resolve into a reset usually combines hot funding for multiple windows, open interest that has stopped expanding or has begun to roll over, a volume profile clustered into the high rather than building below it, and a regime that is not actively supportive of continuation. None of these conditions is a guarantee. The combination tilts the read in a way the funding number alone cannot.

The funding rate plus open interest scanner article on the blog walks through the same combination from the other direction, treating funding and open interest as a pair rather than as two separate columns. The frame is the same; the entry point into the article is just different.

A small structural detail that is worth keeping in mind: even when the conditions favour a reset, the timing of the reset is rarely obvious in advance. The setup describes the conditions that increase reset probability; it does not describe when. A trader who needs to be right about timing as well as direction is taking two risks at once, and funding alerts that imply they can solve both are overstating what the column does.

What context kills it

The funding fade gets killed quickly when the wider market is supportive. A BTC tape that is trending up with broad participation rewards continuation, not reset. Breadth across the perp universe that is widening tells the trader that the move has structural support beyond any single ticker. A volume profile that keeps building under the price implies the move is being accumulated, not chased. Hot funding inside that environment is still hot funding, but the right read is "crowded continues" rather than "crowded resets".

The reading the crypto regime article on the blog explains how SENTINEL composes the regime read, and why it sits above any single ticker decision. Funding alerts that ignore the regime are loud in every tape and useful in none of them.

Funding cycles vs funding spikes

A funding spike is a single window where the rate prints unusually high or low. A funding cycle is several consecutive windows that agree on direction. The two shapes describe different things and produce different reads. A spike is often noise: a brief mark-price deviation, a temporary positioning imbalance, or a flow event that does not persist. A cycle is a position book that has been one-sided for hours, not minutes, and has been paying for the privilege the whole way.

Most threshold-based funding alerts fire on the spike because the spike is the easiest event to detect. The cycle is the more informative signal but requires the scanner to remember the last several windows instead of just the most recent one. A scanner that ranks funding by the cycle rather than the spike will fire less often and miss fewer cycles in exchange. Both behaviours are choices; the operator should be honest about which one they made.

A useful Bybit funding alert format usually combines both. It surfaces the spike for awareness, but escalates to a CORE-level observation only when the spike sits inside a cycle that the rest of the factor stack also agrees with.

Funding arbitrage: not the same as a fade trade

Some traders search for Bybit funding rate alerts because they are building a delta-neutral funding arbitrage strategy rather than a directional fade. The two workflows are very different. Delta-neutral funding arbitrage holds spot and shorts the perp (or vice versa for negative funding), aiming to collect the funding transfer while hedging the price exposure. The risk is not directional; it is execution slippage, hedge basis risk, and exchange counterparty risk.

A funding alert built for arbitrage cares about persistence, depth, and the cost of borrowing the hedge leg. A funding alert built for a fade trade cares about whether the crowd is about to break. The two products look superficially similar and serve very different jobs. SENTINEL is built for the second job, not the first; an arbitrage workflow needs a different toolset and a different risk model entirely.

How SENTINEL frames funding alerts

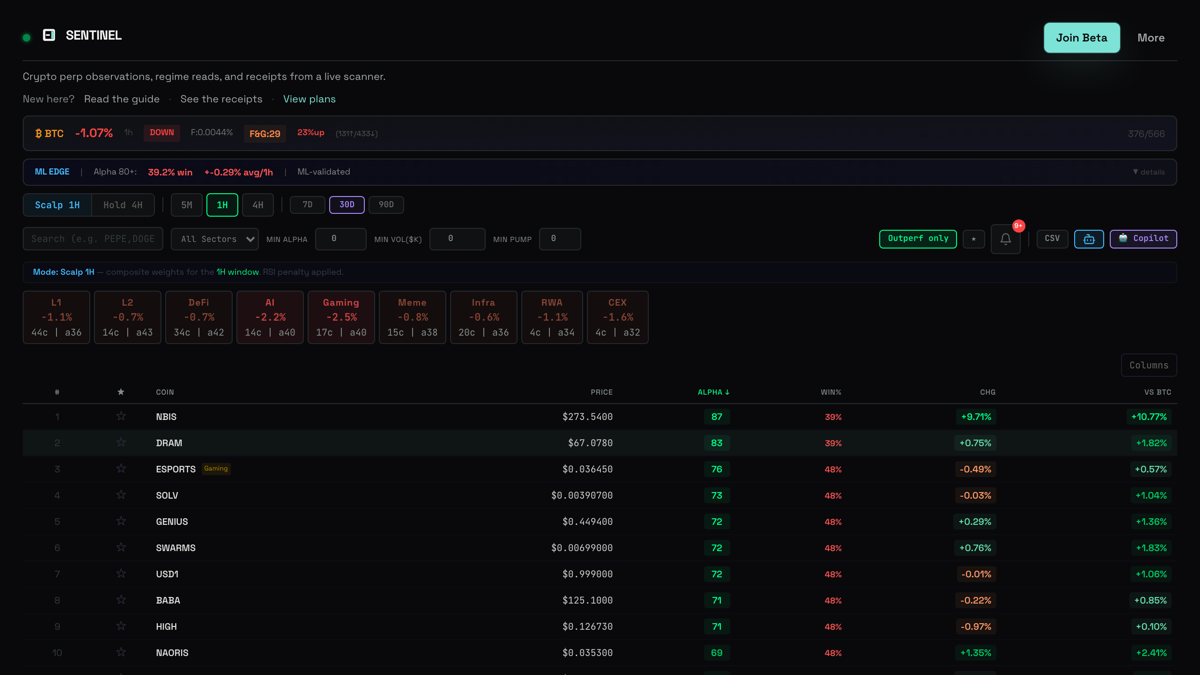

SENTINEL does not ship a "funding crossed threshold" alert as a standalone product. Funding is one column inside the broader factor stack alongside momentum, volume ratio, open interest, RSI, liquidation pressure, and the cross-market regime read. Observations only escalate into a Telegram CORE alert when the columns agree and the regime gate allows it.

That posture deliberately ships fewer alerts than a typical threshold-based product. The trade-off is that each one carries the surrounding context attached, which is the part of the read that decides whether the funding number is actually informative for this particular setup. The Bybit perp scanner factor stack article on the blog walks through the column interactions.

Subscribers who join SENTINEL specifically for funding context sometimes expect a high-volume feed of funding events. The actual feed is quieter than that, because most isolated funding events do not survive the column-agreement check. The trade is fewer notifications in exchange for more signal per notification, and the receipt page is the surface that lets a trader decide whether that trade matches their workflow before paying for it.

A short audit checklist for funding alert products

Most funding alert products are honest about delivery and silent about context. A short checklist separates the useful ones.

- Does the alert include open interest direction at the time of firing?

- Does it report the volume profile, or just the funding number?

- Does it cross-check the broader market regime?

- Does the operator publish how previous funding alerts actually resolved?

- Does the language stay descriptive, or does it tip into "guaranteed fade" framing?

Funding across exchanges: is the cycle real or local

A funding cycle that only shows up on one exchange is a different read from a funding cycle that shows up across the major venues simultaneously. A Bybit-only crowded regime can resolve quickly if other venues are showing calmer funding on the same contract; the imbalance reflects venue-specific positioning rather than a universe-wide view. A cross-venue crowded regime is harder to dismiss because the entire market is leaning the same way.

A useful funding workflow keeps both reads in scope. SENTINEL is primarily a Bybit-focused scanner, but cross-venue funding context is worth checking before acting on any single-venue crowded read. The simplest way to do this is to compare the funding sign and magnitude on the top liquid perp on at least one other major venue at the same time the Bybit alert fires. If they disagree, the crowded read is venue-specific; if they agree, the read is broader and slower to resolve.

Cross-venue checks are also useful in the other direction. A Bybit funding cycle that looks moderate but agrees with a stronger cycle on another venue is often understated by the Bybit-only number. The universe of paying longs (or shorts) is larger than the Bybit read implies, and the reset risk scales with the broader universe.

Receipts before the Telegram trial

SENTINEL keeps a public CORE receipt window on the performance page, fed by https://sentinelresearch.app/api/scanner/tier-performance?mode=live. Receipts cover scanner observations rather than funding events specifically, but the discipline is the same: sample size visible, losing rows visible, no curated screenshots. That surface is meant to be read before the Telegram trial, not after.

Receipts are not promises. They are the inspectable record a trader can audit at the timestamp they care about, instead of relying on a sales thread or a recurring billing arrangement.

Risk boundary

SENTINEL is a research and observation tool. It does not place trades, manage position size, set stops, manage leverage, or offer financial advice. Funding rate alerts are easy to over-trade because the column is simple and the threshold logic is satisfying. Treat every funding observation as information, not as an instruction.

Bybit perpetual futures are leveraged products and can lose more than the margin posted on a single trade. Read the risk disclosure before using the Telegram beta, and never let a single column define risk.

Common questions

How does Bybit funding actually settle?

Funding settles every eight hours and is calculated from the spread between the perp mark price and the underlying index, with an interest-rate adjustment baked in. Positive funding means longs pay shorts; negative funding means shorts pay longs. The size of the payment grows when the perp deviates further from the index.

Is collecting funding a free yield?

No. A trader collecting funding on the short side of a hot positive funding regime is taking on the risk that the move continues against them long enough that the funding income does not cover the position's drawdown. The same applies in reverse for long-side traders collecting negative funding during a panic.

Why does the simple "fade the crowded side" trade fail in practice?

Funding can stay elevated for long stretches when the underlying narrative is strong, open interest can keep building, volume can support continuation, and breadth across the rest of the perp universe can be wide enough that the move has structural tailwind beyond positioning. The funding signal alone is one column.

What context makes a funding fade actually tradeable?

Hot funding for multiple consecutive windows, open interest that has stopped expanding or has begun to roll over, a volume profile clustered into the high rather than building below it, and a regime that is not actively supportive of continuation. The combination tilts the read; the number alone does not.

What is the difference between a funding spike and a funding cycle?

A spike is a single window where the rate prints unusually high or low and is often noise. A cycle is several consecutive windows that agree on direction — a position book that has been one-sided for hours, not minutes, and has been paying for the privilege the whole way.

Is funding arbitrage the same as a funding fade trade?

No. Delta-neutral funding arbitrage holds spot and shorts the perp (or vice versa for negative funding), aiming to collect the funding transfer while hedging the price exposure — risk is execution slippage, hedge basis risk, and exchange counterparty risk. A fade trade cares about whether the crowd is about to break. The two products look similar and serve very different jobs.

Try it live

Connect wallet first, then continue with Telegram to unlock trial/Core features.

How this was produced

Every claim was verified against the live SENTINEL codebase and the current product surfaces. This is educational product documentation, not financial advice.