Funding Rate Arbitrage Scanner vs Signal Scanner: Two Different Jobs

A funding rate arbitrage scanner and a funding rate signal scanner share a word but solve different problems. A guide to which tool answers which question, and where each one breaks.

Summary

A funding rate arbitrage scanner and a funding rate signal scanner share a word, but they solve different problems. The first is a yield tool: it ranks pairs where collecting funding by being long one venue and short another is fee-positive. The second is a context tool: it surfaces funding extremes alongside open interest and volume so a directional trader can read whether leverage is crowding into or unwinding from a setup.

A trader who confuses the two ends up either chasing arbitrage with too little capital to make the basis work after fees, or treating a signal scanner as if it were risk-free yield. Both mistakes are common, and both come from the same root: assuming "funding scanner" describes one product. It describes two.

Two scanners that share a word but do different jobs

A funding rate arbitrage scanner is a yield engine. Its job is to find a pair of venues — or a perp-spot pair on a single venue — where the funding rate plus the basis nets out positive after fees. The trader is long on one leg and short on the other; the position is market-neutral on price and collects funding as carry. The scanner ranks opportunities by annualized return, fee model, and funding payment cadence. It is not telling the trader anything about market direction.

A funding rate signal scanner is a context engine. Its job is to surface when funding is moving in a way that flags a directional setup — a positioning extreme, a squeeze configuration, an open-interest unwind. The output is not "collect this yield." The output is "this setup is currently in a configuration that has historically preceded a move, here are the supporting factors, draw your own conclusion." Funding is one factor among several, and the trader takes a directional position based on the full read.

Both kinds of scanner read the same underlying funding rate feed. They differ in what they do with it. An arbitrage scanner sees a funding number and asks "can I be paid to hold this market-neutral position?" A signal scanner sees the same funding number and asks "what is positioning telling me about the next directional move?" Same input, opposite question, different tool.

What a funding rate arbitrage scanner actually does

An arbitrage scanner ranks pairs by basis or annualized funding return, computes fee-adjusted profitability across two venues (or perp-spot on the same venue), and surfaces the opportunities where the math works after maker/taker fees, funding payment cycles, and slippage. The trader puts on both legs, holds, collects funding, and unwinds when the basis converges or the funding flips against the position.

The mechanics demand real infrastructure. The trader needs margin on both venues — capital is locked across two accounts, not one. Each exchange has its own funding cycle (some pay every 8 hours, some every hour, some hybrid), and a basis trade that looks attractive on the average can be unprofitable on the realized payment cadence. Withdrawal lockups during volatility events can strand one leg while the other gets liquidated. Venue counterparty risk is real: the scanner does not price it.

The biggest hidden cost is the funding rate flipping mid-trade. A pair that paid +30% annualized when the position went on can swing to -15% before the trader can unwind. The arbitrage scanner shows the current snapshot; it does not show how stable the funding rate is, and it cannot warn that the underlying positioning that created the basis is about to unwind. That is a signal-scanner question, not an arbitrage-scanner question.

A trader using an arbitrage scanner is taking on operational risk, venue risk, and basis-convergence risk in exchange for funding yield. Done well, it is a low-variance carry strategy. Done badly — undercapitalized, single-venue, ignoring funding stability — it is a leveraged directional bet wearing an arbitrage costume.

What a funding rate signal scanner actually does

A signal scanner reads funding as a positioning indicator. The premise is that the funding rate reveals the cost that leveraged traders are willing to pay to hold a directional position. Extremely negative funding means shorts are paying heavily to stay short; extremely positive funding means longs are paying heavily to stay long. The extreme itself is not the trigger — many names sit at extreme funding for hours without unwinding — but the extreme combined with the open-interest delta tells a coherent story.

The signal scanner pairs funding with open interest, volume ratio against a trailing baseline, and a market-wide regime label. The four factors together form a state machine. Funding is the positioning gauge; OI delta is the flow gauge; volume ratio is the urgency gauge; regime is the conviction gauge. None of them alone is enough. Funding plus OI delta is the minimum viable read.

The output is not a position. The output is an observation: "this name is currently at extreme negative funding with open interest down over the last hour and volume well above its trailing baseline, in a low-breadth down-tape." That observation is pre-trade context. The trader decides whether to act on it, how to size, and where to stop. The scanner does not. The receipt feed that publishes the observations — including the ones that failed to follow through — is the only honest evaluation surface.

When funding alone is misleading

Funding rates can stay extreme for hours or days before any positioning event. A name sitting at a deeply negative 8-hour funding rate is unambiguously crowded short, but "crowded short" does not equal "imminent squeeze." Shorts can pay heavy negative funding for an entire weekend if the directional conviction is strong enough; the cost is real but bearable for a sufficiently positioned trader. The funding extreme is necessary but not sufficient.

The trigger is positioning flow, not the funding level. Funding tells you positioning is crowded. Open interest delta tells you whether positioning is currently building or unwinding. A name at extreme negative funding for six hours with open interest rising over that window means leverage is still building — new shorts are entering despite the cost. That is not a squeeze setup; it is a name that may be about to break to the downside as fresh shorts press the trade.

Flip the same example. A name at extreme negative funding for six hours with open interest falling over that window means shorts are starting to cover. That is the squeeze setup the funding extreme was hinting at; the flow has now turned. The funding level is identical in both scenarios. Only the OI delta separates them. A scanner that reads funding without OI is reading half the picture, and the half it is reading is the half that lags.

This is why the "funding rate alerts" category is more useful as part of a stack than as a standalone product. A high-funding alert by itself is a question; a high-funding alert paired with the OI delta is closer to an answer. The full walkthrough on combining the two lives at /blog/bybit-funding-rate-alerts and /blog/funding-open-interest-scanner.

The signal-scanner factor stack

A complete signal-scanner read uses four factors: funding rate (positioning), open interest delta (flow), volume ratio (urgency), and regime label (conviction). The four combine into a state machine that resolves the question "what is positioning doing right now and is the broader tape going to support it?" Each factor on its own is ambiguous. The combination is closer to coherent.

The state machine has four corners when you cross funding extremes with OI direction. The corners are not equally common, and they are not equally informative, but each one carries a distinct interpretation that a directional trader can use as pre-trade context. The volume ratio scales the urgency of whichever corner is active; the regime conditions how far the move is likely to extend.

Reading the corners together is what separates a usable signal scanner from a funding-rate ticker. A scanner that only shows funding rankings is closer to a leaderboard than a stack. A scanner that publishes the four-factor read alongside the alert lets a trader decide in under a minute whether the setup matches their playbook or not. The decision is the trader's. The scanner is just refusing to hide the inputs.

- Funding extreme + OI rising = crowded; positioning still building, not yet at the unwind.

- Funding extreme + OI falling = unwinding; potential squeeze in the direction opposite the positioning.

- Funding neutral + OI rising = fresh trend; new positioning entering without a funding cost yet.

- Funding neutral + OI falling = exit; positioning leaving without urgency, low-conviction tape.

Why arbitrage and signal scanners can't replace each other

An arbitrage scanner cannot tell a trader the position is about to unwind, because that is not its job. It surfaces the snapshot return of a market-neutral pair; the underlying positioning that creates the basis is treated as exogenous. A trader who uses an arbitrage scanner as a signal scanner is reading a yield ranking as if it were a directional read, and the result is a leveraged directional trade dressed in an arbitrage frame. That is the worst of both worlds: directional exposure with operational complexity.

A signal scanner cannot tell a trader the cleanest market-neutral spread, because that is not its job. It surfaces positioning context; the execution mechanics of capturing the basis (venue fees, withdrawal lockups, funding cadence) are not its domain. A trader who uses a signal scanner as an arbitrage scanner is taking on directional risk with no execution mechanic to capture the funding it surfaces. There is no carry leg. The trade is a directional bet on a positioning read, full stop.

The two scanners also have different failure modes. An arbitrage scanner fails when the basis flips, fees move, or one venue cascades — see /blog/bybit-liquidation-alerts for how a venue-wide cascade can strand the short leg of an arbitrage pair while the long leg liquidates. A signal scanner fails when the factor stack reads as a setup that does not follow through. The first failure is operational and venue-coupled; the second is statistical and tape-coupled. Building one tool to cover both failure modes is a category error.

What to look for in either tool before paying

For an arbitrage scanner, the diligence questions are operational. What is the fee model on each venue, and does the scanner compute fee-adjusted return rather than gross funding? Are the funding payment cycles per exchange disclosed (8-hour vs 1-hour vs hybrid)? Does the scanner model slippage between venues, or does it assume zero slippage? Are withdrawal-lockup realities — the cases where one leg cannot be unwound during a volatility event — flagged anywhere?

For a signal scanner, the diligence questions are evidential. Is the factor stack complete (funding alone is not enough) and is each factor disclosed? Does the scanner publish a receipts feed that includes the misses, not just the winners? Is the regime gated, so signals in incompatible tapes are flagged or suppressed? Is the data computed server-side from raw exchange feeds, or is the scanner just relaying a third-party feed without adding any state?

A scanner of either kind that cannot answer those questions transparently is probably not worth paying for. The cheaper question is "did the scanner publish what its data looked like when it was wrong?" If the answer is no, the scanner is a marketing surface, not a tool. The general framework for free-vs-paid evaluation lives at /blog/free-crypto-scanner-vs-paid-signals, and the same diligence applies whether the product is arbitrage-flavored or signal-flavored.

How SENTINEL sits in this taxonomy

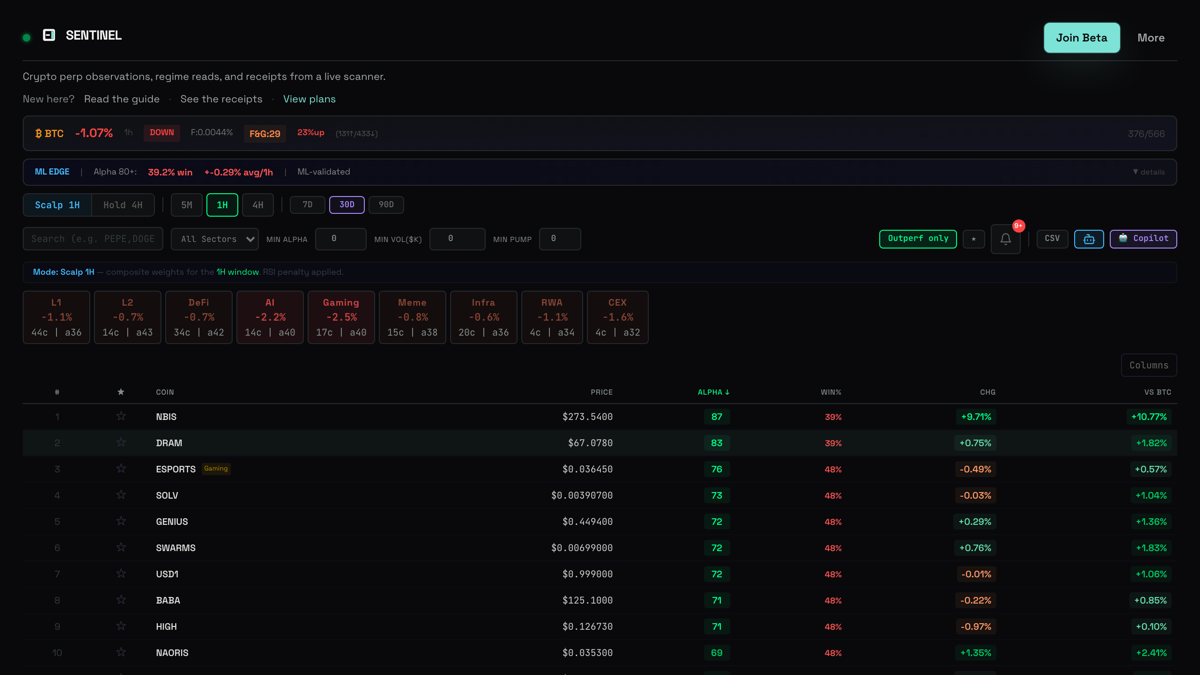

SENTINEL is a signal scanner, not an arbitrage scanner. It scans Bybit perpetual markets server-side and computes a five-factor read — price action, open interest delta, volume ratio, funding rate, and a market-wide regime label (BTC move plus breadth plus volatility) — across the perp universe on a rolling cadence. Funding is one factor; it is not the product. The output is a Telegram observation timestamped against the receipts feed, not a yield ranking and not a position.

The CORE subscriber tiers are sweet and liqsqueeze. Research Lab super extends the surface for traders who want the broader factor configuration with the same receipt discipline after risk acknowledgement. Alpha remains outside CORE/public routing and, where enabled, belongs only to Admin/Research Lab preview evidence rather than live plan marketing. The current CORE-tier rolling track is published at /performance — both winners and misses — so a trader can read what the scanner looked like when it was wrong before deciding whether to start the Telegram trial at /?trial=wallet.

The hosted SENTINEL Trend Pine script is free and open-source, so a trader can run a transparent chart-side trend reference independent of the paid Telegram stream. It is also a signal-context tool, not an arbitrage tool — it surfaces context, not yield. A trader who wants funding arbitrage should be using a dedicated arbitrage scanner alongside, not in place of, SENTINEL.

Funding scanners of either kind — arbitrage or signal — reduce information asymmetry. They do not predict outcomes. They surface a slice of the market that the candle chart cannot show on its own, and they leave the decision with the trader. Bybit perpetual futures are leveraged products; both arbitrage trades and directional trades on perps can produce losses that exceed expectations during cascade events. Read the risk disclosure before using either category of tool.

Try it live

Connect wallet first, then continue with Telegram to unlock trial/Core features.

How this was produced

Every claim was verified against the live SENTINEL codebase and the current product surfaces. This is educational product documentation, not financial advice.